R2 Capital Gains and Losses

The CGT workpapers are designed to assist in calculating gross capital gains or losses, applying the appropriate methods and concessions to reduce the taxable capital gain and help track carried forward capital losses.

Recommended supporting documents:

-

Purchase and sale contracts

-

Settlement statements for property transactions

-

Invoices of expenditure incurred that forms part of the cost base and reduced cost base of the asset

-

Distribution statements from trust and partnership with capital gains received

CGT Event worksheet

Start with this worksheet to calculate the gross capital gain or loss on a single asset.

-

Enter the details of the CGT asset including:

-

Description

-

Asset type

-

Date acquired

-

Date of CGT event

-

Proceeds

-

Indicate if it is an Active Asset

-

-

Indicate whether the CGT event is exempt or qualifies for a roll-over. Select the appropriate exemption or roll-over code.

-

Enter each component of the cost base of the asset, including the date and amount incurred. Then select the appropriate cost base type. The worksheet will automatically calculate the Cost base, Reduced cost base and Indexed cost base based on the details entered.

Deductions claimed includes any costs that have been or can be claimed as a tax deduction e.g. capital works deduction. Enter these amounts as positive values. For assets acquired after 13 May 1997, these deductions will reduce the cost base and reduced cost base.

Modifications, exclusions and adjustments includes market value substitution rule, expenditures recouped and debt forgiveness. Enter increasing amounts as positive values and decreasing amounts as negative values.

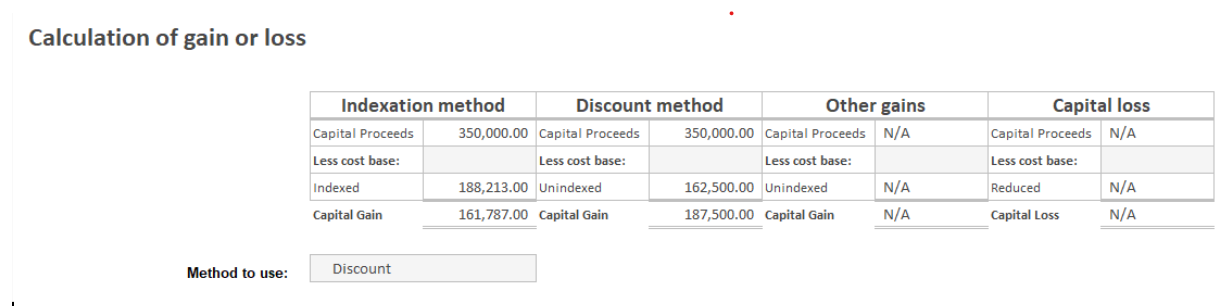

Once all required details are entered, the worksheet will automatically calculate the capital gain or loss using each applicable method. It will then select the method that results in the lowest capital gain and transfer that amount to the Capital Gains and losses summary worksheet. You can manually override this selection if required.

* The discount method in the example above results in a lower net capital gain when the applicable discount is applied. However, if capital losses are available, the indexation method may provide a more favourable outcome.

Use a separate worksheet for each CGT event. Additional CGT event worksheet can be added by specifying the number of CGT events in Workbench.

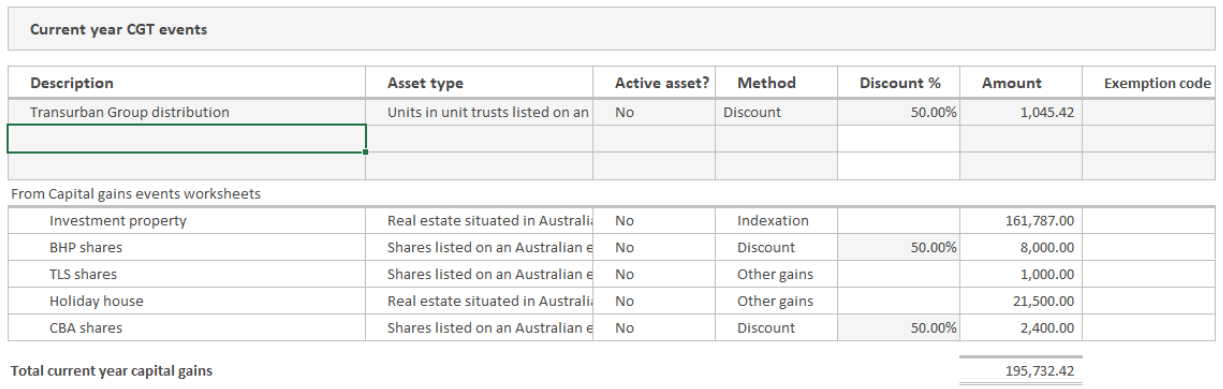

Capital gains and losses summary

Each capital gain or loss completed through the CGT event worksheet will be transferred to the Capital gains and losses summary worksheet. Capital gains and losses that are distributed or calculated externally, can also be entered directly into this summary worksheet under the Current year CGT event section.

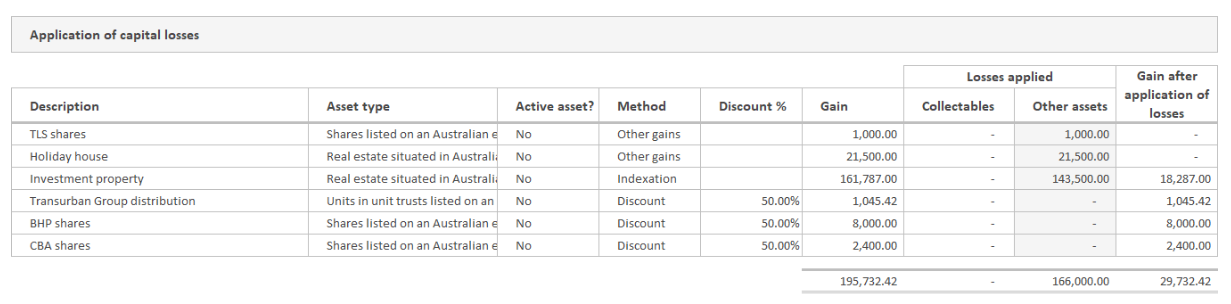

Enter prior year losses in the Available capital losses section to ensure they are tracked and applied correctly.

The worksheet will automatically perform the following actions based on the details entered:

-

Apply the capital losses against current year capital gains in the following order to minimise the net capital gain:

-

Other method

-

Indexation method

-

Discount method

-

-

Apply the applicable CGT discount based on the entity type to calculate the net capital gain for the income year.

-

Calculate the unapplied capital losses to be carried forward, where applicable.

Review the calculated amounts and consider adjusting the method selection to achieve the most favourable outcome in reducing current year net capital gains.